Commercial Snapshot Q4 2024

Commercial Market Snapshot Q4 2024

December 4, 2024

MARKET OVERVIEW

The third quarter’s performance was better than expected and market sentiment continued to climb in the fourth along with broad deal activity. There was general optimism over the return of a “business-friendly” administration to the White House, but there was caution as the industry wondered when Commercial Real Estate (CRE) interest rates would also become friendlier.

Optimism spurred by the .5% interest rate drop by the Federal Reserve (the Fed) in September pushed transaction volume to $68B in Q3, according to CoStar. This activity was off only 18.1% on an annual basis and an advancement of 10.5% from Q2. Also, year-to-date, 12-month rolling sales volume was slightly ahead of 2023. Transactions in Q4 were boosted by investors getting into the market ahead of a full rebound. Indeed, Costar reported that prices picked up for the third month in a row in October and cap rates may be compressing. While Office slightly pulled down the overall Q3 delinquency figure and distress deals rose in September, troubled properties have yet to play a big role.

The four major asset types all saw stronger deal activity in Q3, reflecting stabilizing fundamentals. According to JLL, Industrial has normalized; although vacancy ticked up again, rental rates remain the most attractive of all major asset classes at 3%. Retail rent growth was the strongest since 2008, and the holiday season heralds more in-store shopping and higher spending. Per the National Association of REALTORS®, Multifamily net absorption1 was again over 100% and the vacancy rate crept down. Even the concerned outlook for Office has tempered as net absorption1 became positive in Q3 for the first time in eight quarters.

The Fed’s rate cuts totaled .75% through November, but commercial rates have yet to follow. The 5-2, 7-3 and 10-year4 Treasury rates (which drive commercial rates) were all at least 75 basis points higher in mid-November than in September – a market signal that rates will be higher for longer due to president-elect Trump’s policies.

Trump’s stated goals include cutting corporate taxes – which may foster a larger government deficit while boosting the economy – as well as increasing tariffs broadly, but these factors could relight inflation. For CRE, the new plans may be both dampening and supportive.

For example, CHiPs and IRA allocations, which boosted Industrial development, may be slowed. But onerous tariffs could prompt more onshoring. An emphasis on reducing corporate burdens may inform upcoming debates on capital gains and 1031 exchanges, carried interest breaks and environmental standards. For right now, despite the unknowns, positivity is in the air.

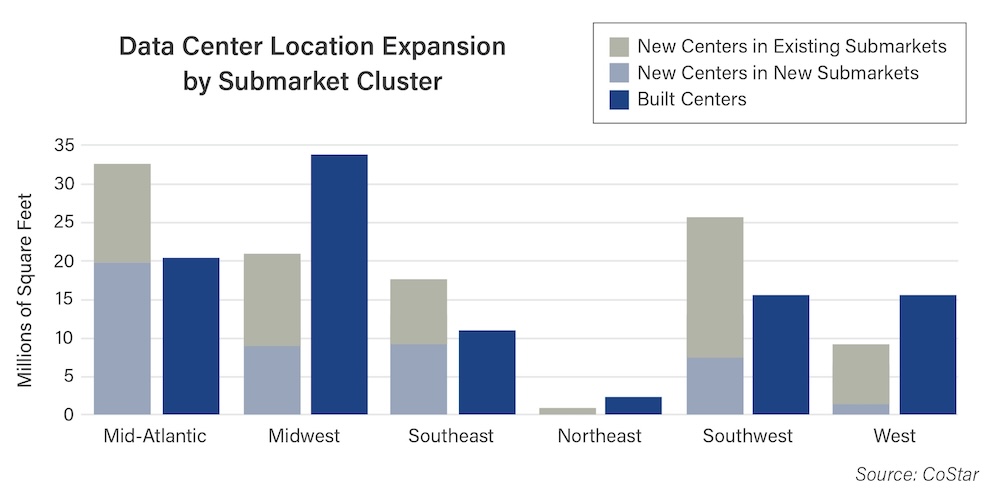

A DEEPER DIVE: DATA CENTERS

For the past year, headlines about Artificial Intelligence (AI), and by extension, data center development, were unavoidable and optimistic. Of late, the costs of data center energy and water usage have come under scrutiny, particularly in some of the largest markets: Virginia, Texas and Georgia. Thus, growth may be easier in new markets.

The chart below details data center placement. New centers in new submarkets could become future clusters. For example, Virginia, which is already the dominant data center cluster in the U.S., will have the most expansion of a new computing footprint. But over half of the additional square footage will be an Amazon facility in Fredericksburg (about two hours south of Washington D.C.). In the West, while few new markets are in development, it is notable that Colorado and Indiana are getting data centers, albeit smaller ones, for the first time. In the Southwest and the Southeast, new construction will more than double the current situation. An Amazon building outside of Jackson, Mississippi, may bring more emphasis there. The Austin, Texas area will remain one of the top places for data centers, although smaller expansions are happening farther afield in Temple and Abilene.

WHAT’S NEXT?

Stay tuned for next month’s Economic Update Q4 2024 to see how the year ends and what 2025 could have in store for commercial real estate.

1 Copyright© 2024 “October 2024 Commercial Real Estate Market Insights.” NATIONAL ASSOCIATION OF REALTORS®. All rights reserved. Reprinted with permission. November 2024, https://cms.nar.realtor/sites/default/files/2024-11/2024-10-commercial-real-estate-market-insights-report-11-07-2024.pdf

2 Board of Governors of the Federal Reserve System (US), Market Yield on U.S. Treasury Securities at 5-Year Constant Maturity, Quoted on an Investment Basis [DGS5], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/DGS5, December 2, 2024.

3 Board of Governors of the Federal Reserve System (US), Market Yield on U.S. Treasury Securities at 7-Year Constant Maturity, Quoted on an Investment Basis [DGS7], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/DGS7, December 2, 2024.

4 Board of Governors of the Federal Reserve System (US), Market Yield on U.S. Treasury Securities at 10-Year Constant Maturity, Quoted on an Investment Basis [DGS10], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/DGS10, December 2, 2024.

Prior Articles

Top Five CRE Markets to Watch in 2026

Top Five CRE Markets to Watch in 2026January 21, 20262026 is projected to be a landmark year for commercial real estate (CRE). Investors aren’… Read More »

Date Center Real Estate: Important Decisions

Data Center Real Estate: Important ConsiderationsOctober 30, 2025While industrial warehouses have expanded rapidly to meet the demands of the… Read More »

Considering Refinancing Your Home

Considering Refinancing Your Home Loan?Have you purchased property since 2022, when mortgage interest rates jumped from the 3% range to almost 8%? If… Read More »

Why Title Insurance Matters

Why Title Insurance Matters: A Cautionary TaleCan you imagine losing your home because someone else has a legal claim to it? It’… Read More »

13 DIY Staging Tips for Home Sellers

13 DIY Staging Tips for Home SellersIf you’re considering selling your home, you may want to think about staging it. According to the National… Read More »

Commercial Snapshot Q1 2025

Commercial Market Snapshot Q1 2025 March 5, 2025MARKET OVERVIEWThe fourth quarter of 2024 marked a return to positive and broad Commercial Real… Read More »

How Hybrid Work is Changing the Office Sector

How Hybrid Work is Changing the Office SectorBy 2025, hybrid work is projected to be the dominant work model for many companies across the nation.… Read More »

Commercial Snapshot Q4 2024

Commercial Market Snapshot Q4 2024December 4, 2024MARKET OVERVIEW The third quarter’s performance was better than expected and market sentiment… Read More »

10 Easy Tips to Create a Healthier Home

10 Easy Tips to Create a Healthier HomeCreating a healthier home is a vital step to enhancing your overall well-being. Your living environment can… Read More »

7 Reasons Homeowners Need Title Insurance

7 Reasons Homeowners Need Title InsurancePurchasing a house is a momentous occasion and likely one of the biggest purchases you’ll ever make.… Read More »